January 22, 2020 Reading Time: 6 minutes

Reading Time: 6 min read

Reading Time: 6 min read

Image Credits: Peggy Pardo/Unsplash

*Angela Huettemann

After a difficult year 2018 and a subsequently strong recovery of both equity and bond markets in 2019, the question is how much upside the global markets as well as the local market have in store for 2020?

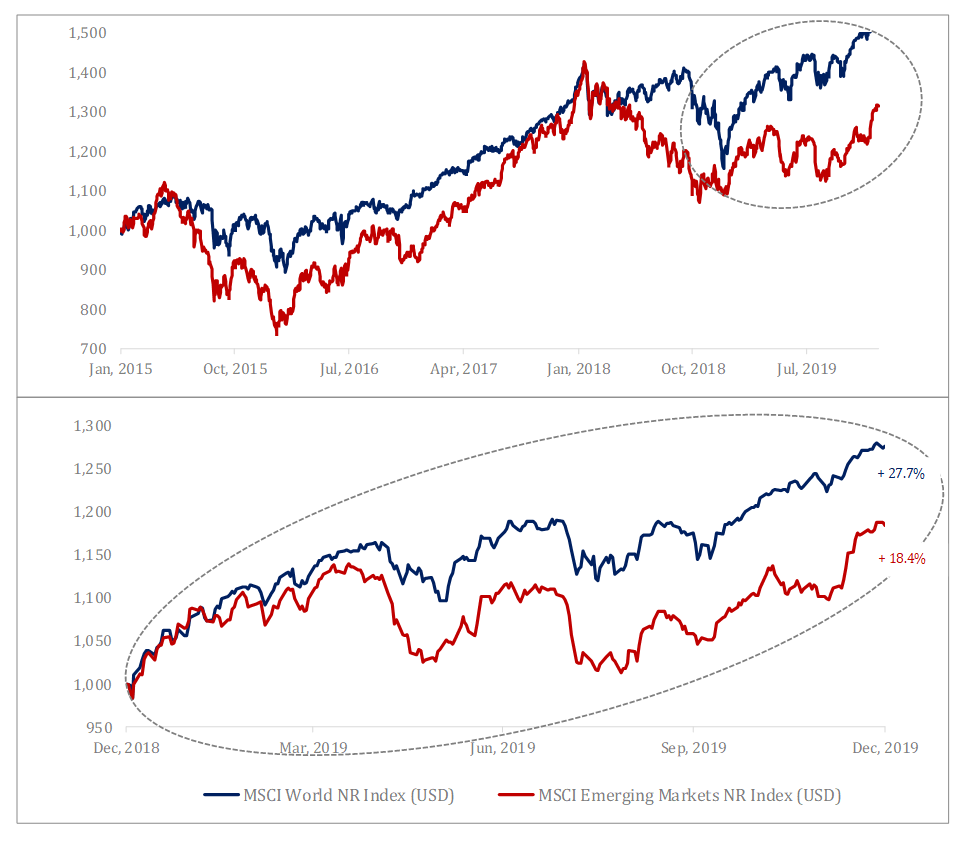

In 2018, markets slumped towards the end of the year, against the backdrop of more restrictive Central Bank policies and a worsening outlook of global economic growth. Developed markets lost 8.7% during the year, posting their worst yearly performance since 2008, whilst emerging markets noted a 14.6% decline, 1 particularly struggling with a strengthening dollar.

In contrast, markets rallied and delivered a stellar performance in 2019, with developed (+27.7%) as well as emerging markets (+18.4%) posting impressive gains.2 It was also a year for tech giants, such as Facebook and Microsoft, which were subject to +50% YoY growth after their stocks had plummeted towards the end of December in the year. 3 Other asset classes, such as fixed income investments saw strong growth during the year, too. Both government (8.0%) and corporate bonds (11.5%) recorded increases in prices and were subject to significant gains 4 , reflecting lingering uncertainty about the world economy and geopolitical tensions.

During the first six months of the year and despite a short-term dip in May, equity markets took a sharp U-turn, and gained strongly following easing trade war tensions and more dovish Central Banks. Markets posted double-digit gains, leading news agencies to believe that it may have been “the best first half for financial markets ever”.5

During the summer, developed markets took a breather after the sharp recovery and moved side-ways against re-emerging trade-war concerns on the one hand, and accommodative central bank policies on the other. Market’s reacted strongly to Trumps’ escalating trade war rhetoric, which destroyed hopes on any nearing resolution of the trade war and triggered a large-scale sell-off in August. Emerging Markets equities were subject to increased volatility over the summer and struggled with a strengthening dollar.

In the US, the Federal Reserve lowered interest rates for the first time since 2008, reducing rates twice over the summer by 25bps respectively. Various emerging market economies, such as India, Thailand,Indonesia and Mexico followed suit by cutting interest rates .6 In Europe, the ECB re-introduced quantitative easing, indicating that the program will continue until inflationary targets have been met, thereby making it country- rather than date-dependent.

*Data indexed at USD $1000 for better visualisation

Source: Historic Development of MSCI World NR Index (USD) and MSCI Emerging Markets NR Index (USD).7

The US treasury yield curve temporarily inverted in August for the second time in 2019, when short-term bond yields surpassed longer-term bond yields, triggering further uncertainty. Such inversions have historically been associated with a pre-recessionary environment. 8 The general uncertainty experienced during the summer and a preference for less-risky investments, led to a temporary shift from growth to value investing. 9

During the last quarter of the year, equities gained additional positive momentum, triggered by renewed hopes on a nearing trade deal between the US and China, ending a more than 16 months tit-for-tat escalation. In Europe and after months of toing and froing, leadership changes and the unlawful prorogation of parliament, markets welcomed the Conservative Party’s landslide General Election victory, hoping for an end to the lingering uncertainty. What’s more, business surveys in the US and Europe indicated slightly improved sentiments. The renewed optimism and risk-off sentiment led to falling bond prices (meaning that yields increased).

2019 has undoubtedly been a successful year for investors, of both global equity as well as global fixed income investments. Contemplating the general increase in uncertainty, the behaviour of bonds (traditionally risk-on investments) has been less so astonishing than the strong gains posted by equities (traditionally risk-off investments). One may therefore wonder if 2019’s equity market highs adequately reflect the underlying fundamentals and economic developments. It appears that investors have already priced in future and additional easing measures.10

Equity markets continued their assured run at the beginning of the year. Their surge did come to a temporary halt, when geopolitical tensions between the US and Iran arose over the assassination of the Iranian Major General Soleimani through a US drone strike. This said, recent rhetoric and actions from both sides seem to have led to a slight de-escalation, with global oil-prices retreating to pre-strike levels and global markets continuing to rise.

Starting the year on already high valuations, a similarly strong run of financial markets to that seen in 2019 seems unlikely. Nevertheless, the bull market may continue for some time, provided the global economy starts to regain momentum, whilst geopolitical risks remain under control. It remains to be seen if weakness in growth has been transitory or more of a permanent and therefore structural nature.

Caution is advisable as a highly leveraged global financial system, as well as the interconnectedness of economies and markets may cause local jitters to quickly translate into global wobbles. Market participants will closely watch various key indicators like global manufacturing output and consumer sentiment alongside political events such as the signing of a potential trade deal between the US and China in mid-January, the trade deal negotiations between the United Kingdom and Europe during the transitory period after Brexit and the Presidential elections in the US later this year.

After having declined 5.6% in 2018, the Sri Lankan market posted a gain of 1.8% in 2019.11 The year was a challenging one for Sri Lanka, which was faced with the Easter Sunday bombings and the resulting fall in tourist numbers as well as slowing GDP growth (2.6% forecasted for 2019, down from 3.2% in 2018).12 As a result, the market temporarily plummeted to its lowest levels since 2012 in mid-May. Experiencing stronger economic headwinds, the Sri Lankan Central bank loosened monetary policy by lowering its key interest rate by 50 bps in both May and August 2019.

With stock markets acting as a barometer of the economy, the pre-election performance of the Sri Lanka CSEALL Index of -0.5% 13 did not come as a surprise. This said, sentiment appears to have improved after the election of Gotabaya Rajapaksa as Sri Lanka’s 7th Executive President in mid-November. Markets welcomed the widely announced tax cuts alongside the announcement of a moratorium on capital repayments for SMEs. Indeed, the market ended the year on a tentative but positive note. Going into the new year, accommodative fiscal policies are expected to provide additional tailwind to the market.

It remains to be seen, whether the supportive fiscal policies are sufficient to trigger sustained economic growth in Sri Lanka. Rating agencies such as Fitch, which has recently downgraded Sri Lanka’s Long-Term Foreign Currency Issuer Default Rating over concerns over the country’s debt sustainability14 , remain cautious about the impact of the widely announced tax cuts on the country’s public debt levels and persisting twin deficit. In a statement following the downward revision, the Sri Lanka’s Central Bank disputed Fitch’s decision, reiterating that the government’s commitment to fiscal consolidation was uncompromised and that the revision did not take into consideration the positive economic growth effect of the reduced tax rates on the one hand and offsetting measures (such as the increase of certain types of taxes and the implementation of measures to curtail government expenditures) on the other.15 It remains to be seen, which net impact the fiscal policies will have on Sri Lanka’s economy in general and local businesses in particular.

Going forward, it appears that addressing macroeconomic imbalances whilst at the same time providing accommodative policies for the private sector are key for improving the operating environment for businesses in Sri Lanka and for renewing investor interest in local businesses.

1MSCI Data. (2020). End of day index data search. [Online] Morgan Stanley Capital International. Data for MSCI World NR Index (USD) and MSCI Emerging Markets NR Index (USD). Available at: https://www.msci.com/end-of-day-data-search [Accessed 12 January 2020].

2Ibid.

3Bloomberg stock quotes. [Online] Bloomberg. Available at: https://www.bloomberg.com/quote/FB:US and https://www.bloomberg.com/quote/MSFT:US [Accessed 10 January 2020].

4Bell, M. (2020). Review of markets over 2019. J.P.Morgan Asset Management. Information on Barclays Global Inflation-Linked and Barclays Global Aggregate – Corporates. [Online] Available at: https://am.jpmorgan.com/de/institutional/library/market-insights-monthly-market-review-december-2019 [Accessed 13 January 2020].

5Jones, M. (2019). The best first half for financial markets ever. [Online] Reuters. Available at: https://www.reuters.com/article/us-global-markets-analysis/the-best-first-half-for-financial-markets-ever-idUSKCN1TT1OR [Accessed 10 January 2020].

6Strohecker, K. & Carvalho, R. (2019). Down, down they go: Emerging central banks deliver most rate cuts in a decade. [Online] Reuters. Available at: https://www.reuters.com/article/us-emerging-rates/down-down-they-go-emerging-central-banks-deliver-most-rate-cuts-in-a-decade-idUSKCN1VN1J2

[Accessed 10 January 2020].

7Supra note 1.

8Leatherby, L. & Greifeld, K. (2019). About when the next recession could happen. Bloomberg.

9Carosa, C. (2019). How you can profit as market shifts from growth to value stocks. [Online] Forbes. Available at: https://www.forbes.com/sites/chriscarosa/2019/10/10/how-you-can-profit-as-market-shifts-from-growth-to-value-stocks/#3644283c6cb7 [Accessed 10 January 2020].

10Stegeman, H. (2019). Partying on a sinking dancefloor. Triodos investment Management. [Online] Available at: https://www.triodos-im.com/articles/2019/economic-outlook-q3-2019

[Accessed 10 January 2020].

11Bloomberg stock quotes. [Online] Bloomberg. Information on CSEALL Index LKR. Available at: https://www.bloomberg.com/quote/CSEALL:IND [Accessed 10 January 2020].

12Asian Development Bank. (2019). [Online] Available at: https://www.adb.org/countries/sri-lanka/economy [Accessed 12 January 2020].

13Bloomberg: CSEALL Index LKR. Performance for 31/12/2018 – 15/11/2019.

14Fitch Ratings. Fitch Revised Outlook on Sri Lanka to Negative; Affirms ‘B’. Fitch. [Online] Available at: https://www.fitchratings.com/site/pr/10105494 [Accessed 12 January 2020].

15Central Bank of Sri Lanka (2020). Sri Lankan authorities strongly dispute the premise of the revision of the outlook by Fitch Ratings. Central Bank of Sri Lanka. [Online] Available at: http://www.treasury.gov.lk/documents/10181/50545/PR+19122019.pdf/2cfa1d78-4459-4ece-9a7e-e0f60ec93cb4?version=1.0 [Accessed 14 January 2020].

*Angela Huettemann is a Research Fellow at the Lakshman Kadirgamar Institute of International Relations and Strategic Studies (LKI) in Colombo. The opinions expressed in this article are the author’s own views. They are not the institutional views of LKI, and do not necessarily represent or reflect the position of any other institution or individual with which the author is affiliated.

24 Horton Place

Colombo 7

Sri Lanka

A think tank engaging in independent research of Sri Lanka’s international relations and strategic interests, to provide insights and recommendations that advance justice, peace, prosperity, and sustainability.